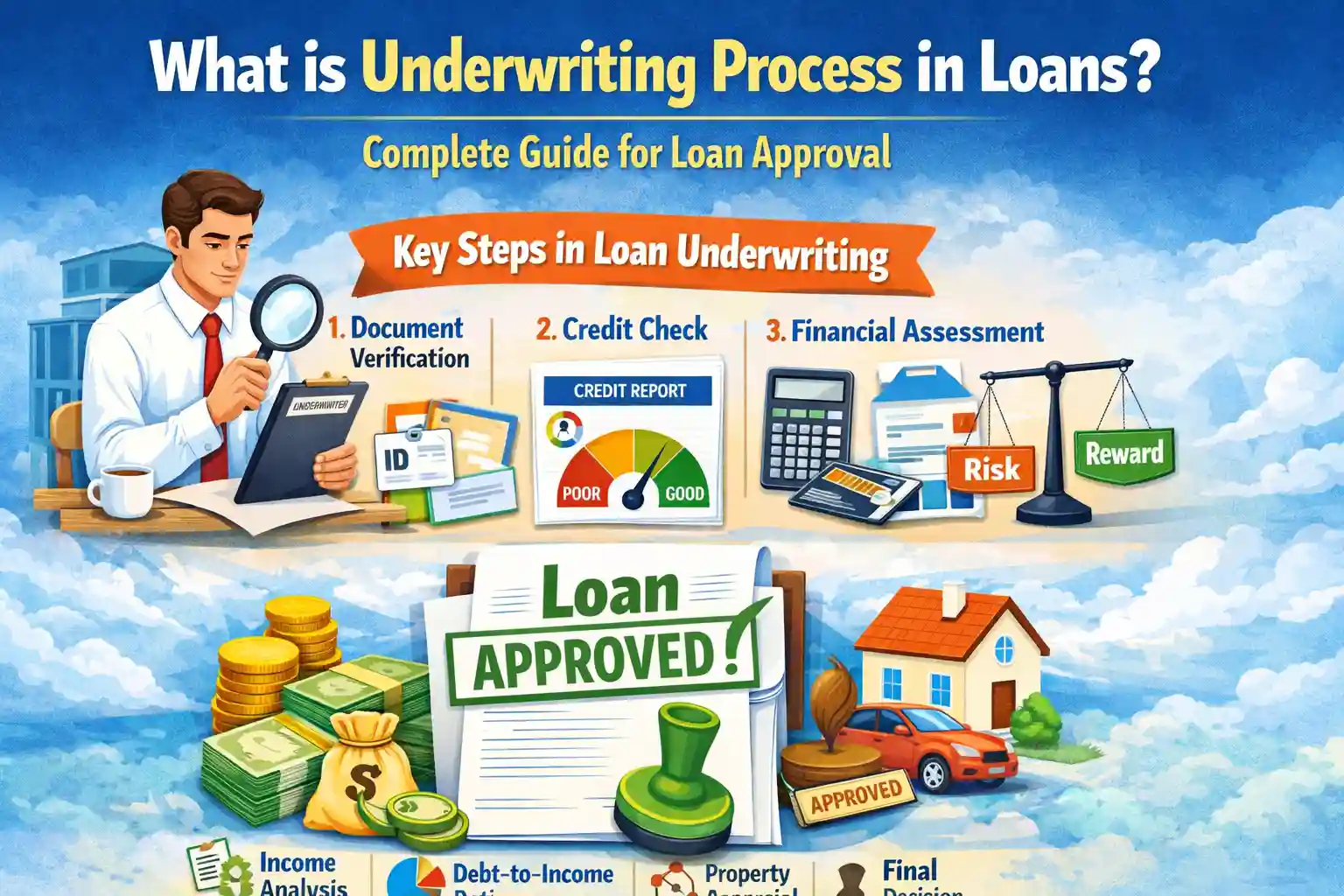

Whenever you apply for a loan, whether it is a personal loan, home loan, or business loan, you might think approval depends only on your salary or documents. However, the actual decision happens through a detailed process called Underwriting.

The underwriting process is one of the most important stages in lending. It helps banks and NBFCs evaluate the risk involved in giving you a loan. Based on this process, your loan may be approved, rejected, or approved with conditions.

In this comprehensive guide, we will explain everything about underwriting — meaning, process, factors, types, real examples, and tips to improve approval chances.

What is Underwriting in Loans? 🧾

Underwriting is the process used by lenders to analyze a borrower’s financial profile and determine their ability to repay a loan.

👉 In simple words: Underwriting is the decision-making process behind loan approval.

It involves checking multiple aspects such as income, credit history, existing obligations, job stability, and banking behavior.

The goal of underwriting is to ensure that:

- ✔️ The borrower can repay the loan

- ✔️ The lender’s risk is minimized

- ✔️ The loan terms are suitable for the borrower

Why Underwriting is Important ⚠️

Underwriting plays a crucial role in the financial system. Without it, banks would face high defaults and borrowers could fall into financial stress.

- 🏦 Protects lenders from bad loans (NPAs)

- 📊 Ensures responsible lending

- 💰 Helps determine interest rates

- 📉 Reduces chances of loan defaults

- ⚖️ Maintains overall financial stability

For borrowers, underwriting ensures that they do not take loans beyond their repayment capacity.

Types of Underwriting 📊

1. Manual Underwriting

In manual underwriting, a credit manager reviews your entire profile manually. This includes checking documents, income proof, bank statements, and credit history.

- ✔️ Detailed evaluation

- ✔️ Suitable for complex cases

- ❌ Time-consuming

2. Automated Underwriting

Automated underwriting uses algorithms and systems to instantly evaluate loan applications. This is commonly used in digital lending platforms.

- ⚡ Fast approval (within minutes)

- 📊 Rule-based decisions

- 🤖 Less human intervention

Most lenders today use a hybrid approach combining both methods.

Step-by-Step Underwriting Process 🔄

1. Loan Application Submission

The process begins when you submit your loan application along with required documents such as:

- PAN card

- Aadhaar card

- Salary slips / ITR

- Bank statements

2. KYC & Document Verification

The lender verifies your identity and address through KYC. This ensures that the applicant is genuine.

3. Credit Score Check

Your credit score (CIBIL) is checked to understand your repayment behavior.

👉 Read more: What is CIBIL Score

4. FOIR Analysis

Your existing EMIs are compared with your income to calculate FOIR. This determines your repayment capacity.

5. Banking Analysis

Your bank statements are analyzed to check:

- Income consistency

- EMI payments

- Cheque bounces

6. Employment & Income Stability

The lender checks job stability, company profile, and salary consistency.

7. Risk Categorization

Based on all parameters, the borrower is classified into risk categories like low, medium, or high risk.

8. Final Decision

The loan is either:

- ✔️ Approved

- ❌ Rejected

- ⚠️ Approved with conditions

Key Factors Checked in Underwriting 🔍

| Factor | Details | Impact |

|---|---|---|

| Income | Salary or business income | Determines loan eligibility |

| CIBIL Score | Credit history | Higher score = better approval |

| FOIR | EMI vs income | Lower ratio preferred |

| Employment | Job stability | Stable job increases chances |

| Bank Statement | Cash flow & spending habits | Shows financial discipline |

Real-Life Example of Underwriting 📌

Let’s understand underwriting with an example:

- Salary: ₹40,000

- Existing EMI: ₹18,000

- CIBIL Score: 680

In this case:

- FOIR is high (~45%)

- CIBIL is average

👉 Result: Loan may be approved with lower amount or higher interest rate.

Common Reasons for Loan Rejection 🚫

- ❌ Low credit score

- ❌ High FOIR

- ❌ Multiple loans

- ❌ EMI bounces

- ❌ Unstable job

How to Improve Underwriting Profile ✅

- ✔️ Maintain CIBIL above 750

- ✔️ Keep FOIR below 50%

- ✔️ Avoid EMI bounces

- ✔️ Close small loans

- ✔️ Maintain stable income

Underwriting in Different Loan Types 🏦

Personal Loan

Focus on income, credit score, and FOIR.

Home Loan

Includes property verification and long-term repayment ability.

Business Loan

Focus on business cash flow and financial statements.

Manual vs Automated Underwriting 📊

| Feature | Manual | Automated |

|---|---|---|

| Speed | Slow | Fast |

| Accuracy | High | Rule-based |

| Use Case | Complex cases | Instant loans |

Conclusion 🎯

Underwriting is the most important step in loan approval. It ensures that loans are given responsibly and reduces financial risk.

Understanding underwriting helps you:

- ✔️ Improve loan approval chances

- ✔️ Avoid rejection

- ✔️ Get better loan terms

Before applying for a loan, always check your credit score, FOIR, and income stability.

Explore more: TechFinserv Blog